-

Risk Advisory

Security for your business

-

Digital advisory & IT consulting

Mastering digitalisation together

-

Operational Advisory

Solidifying and supporting transformation

-

Deal Advisory

We’ll advise you on national and international transactions

-

Valuation & economic and dispute advisory

We’ll value your business fairly and realistically

-

Financial Advisory

Optimising financial structures

-

Tax for businesses

Because your business – national or international – deserves better tax advice.

-

Tax for financial institutions

Financial services tax – for banks, asset managers and insurance companies

-

Employment law

Representation for businesses

-

Commercial & distribution

Making purchasing and distribution legally water-tight.

-

Inheritance and succession

Don’t leave the future to chance.

-

Financial Services | Legal

Your Growth, Our Commitment.

-

Business legal

Doing business successfully by optimally structuring companies

-

Real estate law

We cover everything on the real estate sector, the hotel industry, and the law governing construction and architects, condominium ownership, and letting and renting.

-

IT, IP and data protection

IT security and digital innovations

-

Mergers & acquisitions (M&A)

Your one-stop service provider focusing on M&A transactions

-

Sustainability strategy

Laying the cornerstone for sustainability.

-

Sustainability management

Managing the change to sustainability.

-

Sustainability reporting

Communicating sustainability performance and ensuring compliance.

-

Sustainable finance

Integrating sustainability into investment decisions.

-

International business

Our country expertise

-

Entering the German market

Your reliable partners.

Update: Financial support for businesses

14 Aug 202014. August 2020

The Corona assistance package for commercial and freelance companies are the largest aid package in the history of the Federal Republic of Germany. So far, corona aid with a volume of 63.7 billion euros has been approved (as of 28.07.2020).

The following chart shows how this is distributed

Source: https://www.bmwi.de/Redaktion/DE/Infografiken/Wirtschaft/corona-hilfen-fuer-unternehmen.html

In this update, we would like to present to you the measures of the Economic Stabilisation Fund (“Wirtschaftsstabilisierungsfonds” or “WSF”) which have now been concretised by the Federal Ministry of Economics and Energy (BMWi), in particular the pillars (can be combined):

- Federal Government guarantees to secure loans including credit lines, and capital market products in the debt capital area.

- Recapitalisations for the direct strengthening of equity capital.

The measures of the WSF are only available for companies in the “real economy” (“Realwirtschaft”) whose existence would be endangered if they had a considerable impact on the business location (technological sovereignty, security of supply and critical infrastructure) or the labour market in Germany. These pillars are specifically designed by the

Guarantee for bank loans

- Only possible if KfW special programme and guarantee programmes of the federal states or large guarantee programmes (federal/federal state guarantees) are not applicable

- Eligible applicants are only large companies (no SMEs) and companies that are not classified as "companies in difficulty" according to the EU definition

- Intended use: investments and working capital

- Term max. 5 years

- Maximum 90% default guarantee

- Various restrictions and conditions on existing financing and distribution policy

Silent partnerships up to 100 million euros

- The aim is to restore equity capital (before Corona) and balance sheet structures for the complementary raising of debt capital on the credit and capital markets.

- Eligible applicants are only large companies (no SMEs) and companies that are not classified as "companies in difficulty" according to the EU definition

- The silent partnerships take the form of typical silent partnerships

- Intended use: investments and working capital

- Term:

- Large enterprises: max. 7 years (bullet maturity) / 10 years (in case of loss recovery)

- Listed companies: max. 6 years (final maturity)

- Fixed interest rate increases with maturity (initially 4.0% to 7.0% p.a. in the seventh year of maturity)

- Various restrictions and conditions on existing financing and distribution policy and prohibition to pursue an aggressive expansion strategy

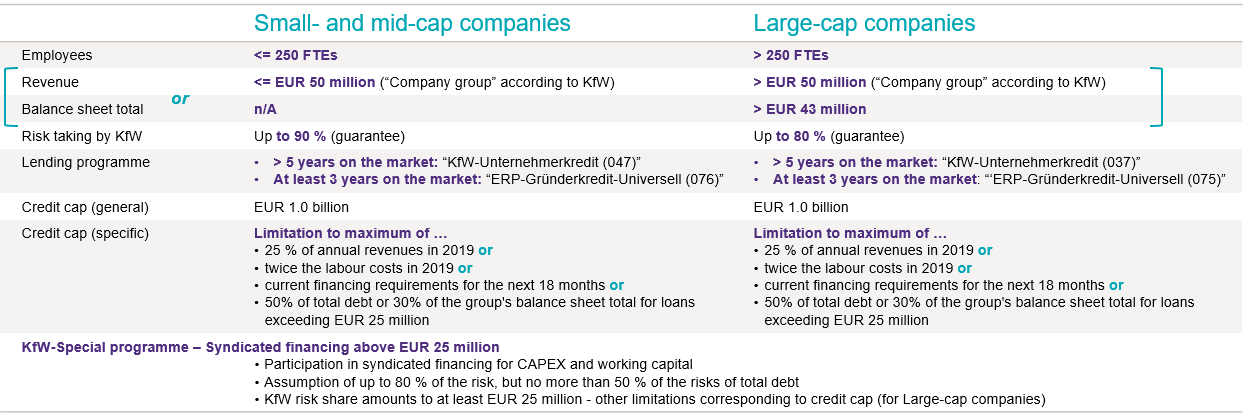

Please find an overview of the further design in the adjacent presentation.

14 May 2020:

On 14 May 2020, KfW published new leaflets for the "KfW-Unternehmerkredit" and the "KfW-Gründerkredit" with the following change:

- The maximum loan amount per group (as defined by KfW) was reduced from EUR 1.0 billion to EUR 100.0 million

Note: There are no transition periods. Applicants for loan amounts above EUR 100.0 million have to apply for the KfW programme “Direktbeteiligung für Konsortialfinanzierung" or, if applicable, the Economic Stabilisation Fund (“Wirtschaftsstabilisierungsfonds” or “WSF”), which can be applied for via the Federal Ministry of Economics and Energy (“Bundesministerium für Wirtschaft und Energie” or “BMWi”) (soon).

27 April 2020:

In the context of the development of the COVID-19 pandemic, the German government enhanced the already adopted measures and decided on additional emergency relief measures which are mainly implemented by the KfW [German state-owned development bank]. Hence, we provide an update of our article dated 23 March 2020. We look forward to your feedback. Let’s get in touch.

State guarantees / Guarantee banks

- Adjustment of guarantees to 90 % (previously 80 %), assumption of liabilities and adjustment to the documentation required

- Specification of the conditions in the relevant KfW-leaflets

- Major regional differences persist

New KfW-“Schnellkredit” 2020

- KfW-“Schnellkredit” with an assumption of liabilities of 100 percent implemented on 15 April 2020

- Available to all companies with more than 10 employees

- Credit volume per company limited to 25% of its 2019 turnover (max. credit volume EUR 500,000 for companies with up to 50 employees and EUR 800,000 for companies with more than 50 employees respectively)

- Credit approval process does neither involve a credit risk assessment by the bank nor by the KfW

- The KfW-“Schnellkredit” will be granted at an interest rate of 3 percent and a 10 years term

- But: partially "hard restrictions": among others, limitation of the remuneration of the company's managing directors to EUR 150,000

Adjustment of the KfW Special Programme 2020 (corona liquidity support)

- Omission of the previously required going concern qualification

- Specification of the requirements regarding the “sufficiency of financing” (“Durchfinanzierung”)

- Specification of the definitions of covenants and deferral agreements ("loss of creditworthiness")

- Extension of the eligible price/risk category I (probability of default (PD) <= 10.0% and recoverable collateral 0% ≤ 40%)

- From now on, loans up to EUR 800,000 with a maximum term of 10 years are available. A maximum term of 6 years applies to larger credit volumes, with a grace period of up to 2 years

- Simplification of the fast track procedure - for loans between EUR 3-10 million - the submission of no more than a single relevant document by the bank is required. The KfW conducts the risk assessment for the bank, the process does not involve additional credit risk assessment by KfW or the submission of additional documents

- Distribution of profits and dividends is not permitted during the term of the KfW loan – customary remuneration to business owners (natural persons) are not subject to this provision however

These presentations include an overview of the topics and a checklist for the application.

Act now: We recommend companies conducting the following quick check:

- Liquidity analysis, including simulation of the expected liquidity requirements to be covered by new measures as well as assessment of the own situation as of 31 December 2019 (= resilience of the business model before and after the COVID-19 crisis)

- Analysis of the existing financing contracts with regard to anticipated and actual reasons for termination in 2019, if any, under special consideration of breaches of financial covenants

- Update/preparation of the usual documentation / figures for banks (including annual financial statements, financial forecasts)

- Early communication with at least two (core) banks to obtain information concerning the willingness to grant/increase credit facilities; especially with regard to the banks’ ability / willingness to assume liability of the residual liability

- Evaluation of possible utilisation of currently unused credit facilities and "parking" of liquidity at other banks

Our experts are happy to assist you in case you have further questions or need advice.

Your contact persons:

Markus Paffenholz

Partner

T: +49 211 9524 8263

E: Markus.Paffenholz@wkgt.com

Stefan Lengermann

Senior Manager

T: +49 211 9524 8483

E: Stefan.Lengermann@wkgt.com

Jan-Philipp Bülow

Senior Manager

T: +49 40 43218 6239

E: Janphilipp.Buelow@wkgt.com

Dr. Gunter Franzke

Partner

T +49 30 890 482 455

E gunter.franzke@wkgt.com

Thomas Leschke

Senior Manager

T +49 30 890 482 451

E thomas.leschke@wkgt.com